As ESG continues to dominate conversations and global media, the rise in consumer demand for ESG investment solutions is becoming more apparent, and the need for the industry to prepare for those client conversations and to be able to propose suitable investment products is becoming paramount.

Research by the Responsible Investment Association Australia (RIAA) found that

- 90% of Australians expect their superannuation and other investments to be invested responsibly and ethically

- 9 in 10 Australians believe that their financial adviser should provide responsible/ethical investment options, and

- 86% believe that their adviser should ask them about their interests and values in relation to investments.

Furthermore, a NextWealth ESG tracker study identified that the overwhelming majority of financial advice professionals (rising from 70% to 80% in the past year) expect to see continued increase in assets invested in ESG funds and solutions.

They explain that smaller firms are more likely to have a higher number of client assets invested in ESG solutions and seem to be more bullish on their expected increase in allocation to ESG over the coming year.

In discussion with small advice businesses, they saw some evidence of firms adopting ESG as a special focus for their practice and marketing their ESG credentials as a point of difference to current and prospective clients.

They also believe that once a small firm settles on an ESG stance and solution that they are confident in, they may be more likely to transition all their clients across to this new proposition. Other evidence suggests that adoption will rise once better solutions are available. This typically covers solutions for the investment proposition, risk profiling and on-going reporting.

The most important driver of adoption, however, is regulatory change.

This is not the case in Australia, where ESG investment and reporting is fundamentally investor led with regulation needing to catch up.

Despite the uncertainty and lack of regulation, in just a couple of decades, the concept of ethical or ‘green’ investing has grown from a few disparate funds to an industry in itself with billions being invested by large fund houses.

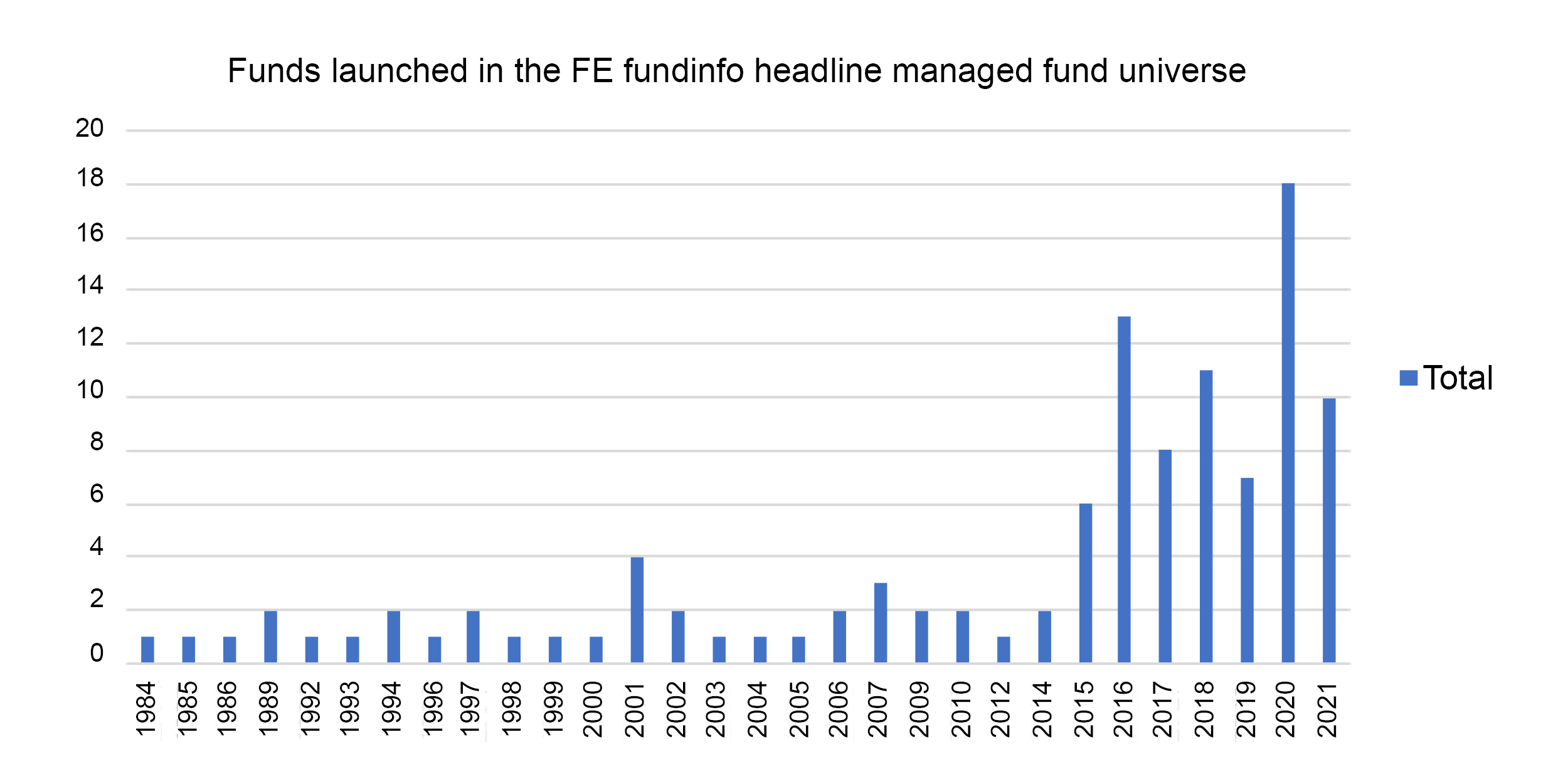

Data from FE fundinfo shows that of the 109 headline funds in Australia that label themselves as Ethical / Sustainable / ESG, 49% were launched within the last 5 years, and 32% within the last 3 years.

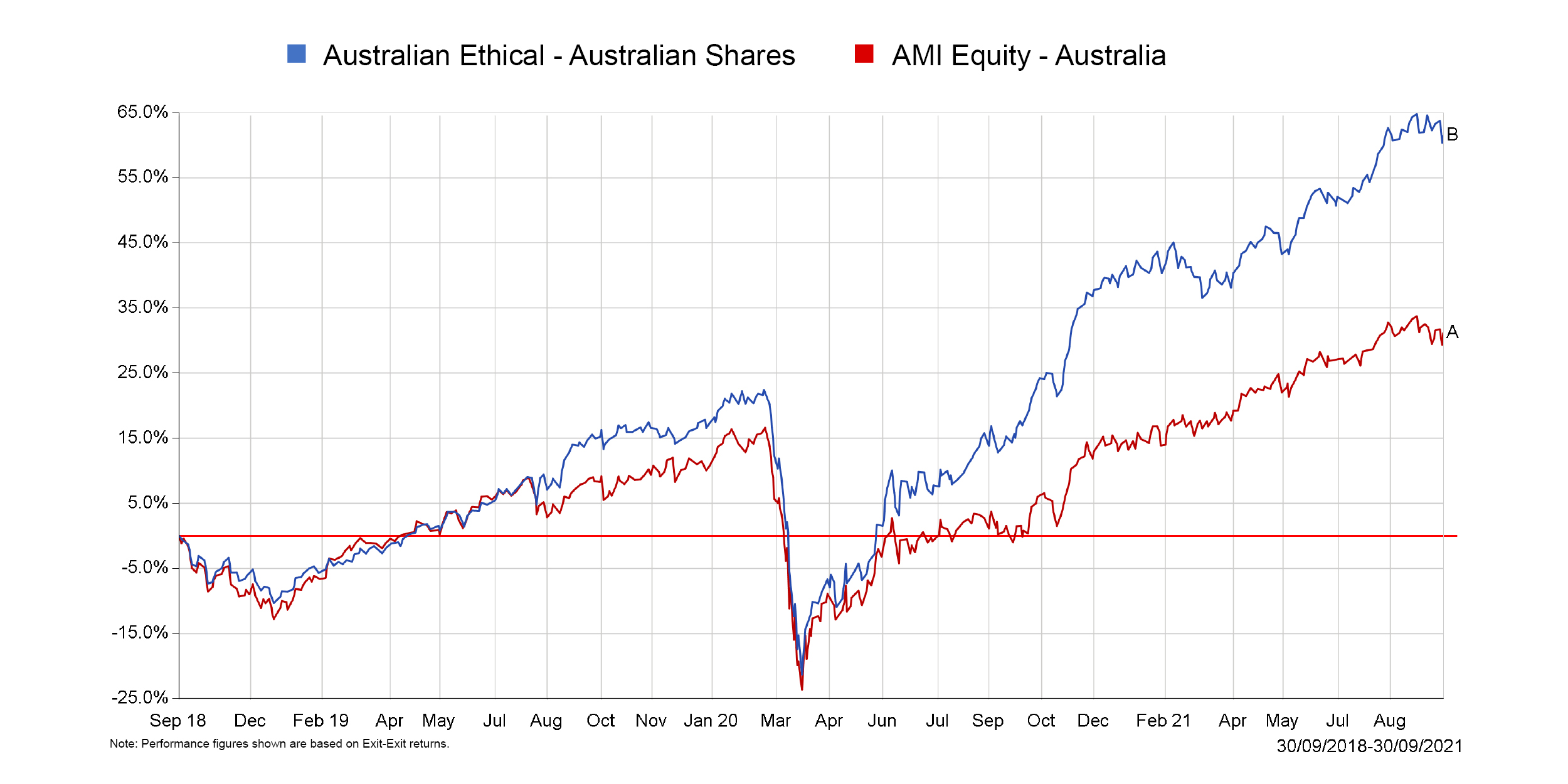

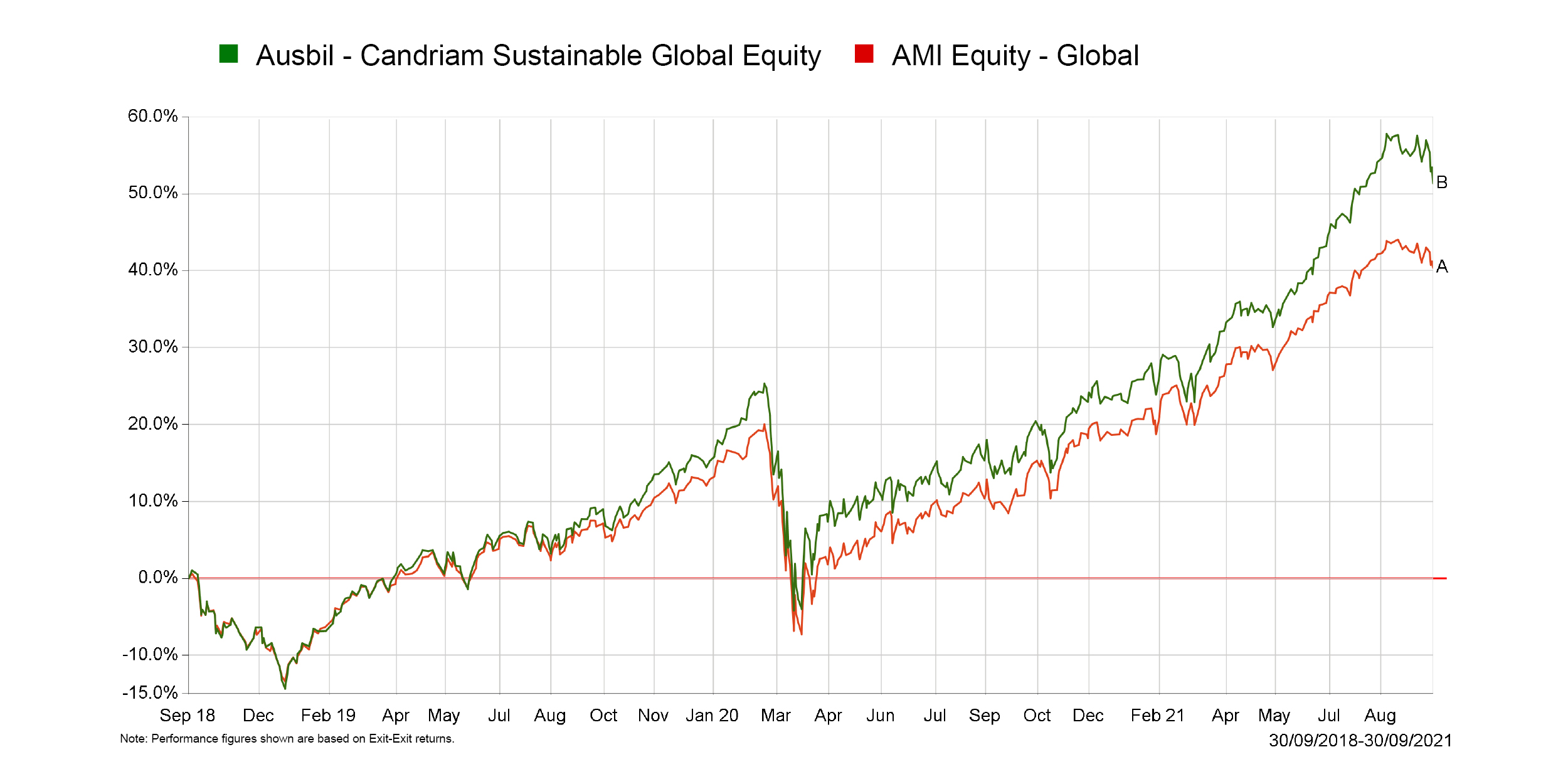

Evidence has steadily accumulated to support the conclusion that responsible investing can deliver strong, risk-adjusted returns for investors and that investors do not need to sacrifice returns in order to reach ethical investment goals.

Examples of the outperformance of ESG funds over a 5- and 3- year time horizon can be seen in the following data from FE Analytics:

Regulations across the EU and Asia

Given this growing demand and global pressure on businesses to implement strategies to achieve net zero targets, countries such as the UK and broader Europe have begun to implement regulations such as the Task Force on Climate-related Disclosures (TCFD), Sustainable Finance Disclosure Regulation (SFDR) and the Regulatory Technical Standards (RTS).

More specifically, TCFD aims to improve and increase the reporting of climate-related financial information including risks and opportunities presented by rising temperatures, climate-related policy, and emerging technologies. SFDR divides products into various categories that require mandatory disclosure on how sustainability risks are incorporated into the investment decision making. RTS on the other hand consists of a template that lists several principal adverse sustainability impact indicators including 32 mandatory indicators around climate and the environment; social, employee and human rights; anti-bribery and anti-corruption issues. RTS requires that advisers publish a statement on their website outlining how they select the products they recommend to clients and how they use information available to them by product providers.

Most recently, the European ESG Template (EET) was developed as part of the EU’s SFDR regime and aims to provide the required data set for all funds to explain their ESG characteristics with differing levels of reporting depending on a fund’s definition. This template will help facilitate the exchange of ESG data between market participants and aid compliance with European financial market regulation.

Looking closer to home, China has recently adopted a Common Ground Taxonomy in order to align the EU and China taxonomies. Covering 61 activities across 6 sectors, this principles-based approach outlines overlap to improve interoperability between regions to enable better data and more consistent regulation across jurisdictions to produce relevant investor information.

Regulatory landscape in Australia

Until now, Australia was the only major fund market with no implemented portfolio holdings disclosure regime. Disclosure is still voluntary and Australian funds do not need to ascribe to any standardised templates or data sets for construction, disclosure, or reporting.

While APRA’s final climate risk prudential guidance and vulnerability assessment does not provide clear guidelines disclosure and reporting of ESG funds, the introduction of ASIC’s greenwashing review demonstrates that the regulator understands the importance of this emerging sector.

Despite the lack of regulation in this space, an in-depth analysis of ESG reporting across ASX200 companies by PwC found that ESG reporting in Australia is moving in the right direction, albeit slowly. They found that while 70% of ASX200 companies have a sustainability strategy, 21% have sustainability as an integral part of their core strategy. 36% of companies have a net zero target and 38% provide short-, medium-, and/or long-term timelines for ESG targets.

Furthermore, the report states that there was a 9% increase in the number of companies getting their ESG reporting assured by external providers which clearly shows that these companies understand the necessity for accurate reporting and disclosure.

Where is Australia headed?

Following the decision whereby the International Sustainability Standards Board (ISSB) will sit alongside the International Accounting Standards Board (IASB), these bodies will seek to provide global benchmarking and streamlined frameworks. Australia has been advised to ‘get on board’ or risk reputational damage of the local financial market amid global capital markets.

There has also been recommendation that Australian regulators align ASX listed companies to TCFD. To date, the Task Force consists of 32 members from across the G20, and it would be remiss if we were left behind.

Given the rise in consumer demand for ESG investment solutions and the mounting global pressure for businesses (and countries) to meet net zero targets in a short few years, it makes sense to introduce processes that will not only allow for standardisation and transparency across jurisdictions, but also provide certainty and confidence by advisors in the recommendation of these financial products.

While we are not there yet, we believe that it’s only a matter of time before Australian regulators introduce a mandatory reporting and disclosure regime.

How can we help?

To find out how we can help you stay ahead of the curve, visit our ESG Solutions page.

White Paper: ESG Investing - Where to for Australia?

Read about ESG investing in more detail, in the context what it means to investors, what regulations are in place in other parts of the world when it comes to ESG-related disclosure, and where the Australian investment industry may end up sooner than we think.

Webinar: Tools for Advisers to have engaging ESG conversations with clients

If you missed our session in the IMAP InvestTech virtual conference, watch the recording.