A centralised retirement proposition brings many benefits to both advisers and their clients - it gives an advice structure and plan for when clients need to take an income in retirement and helps to mitigate some of the associated risks.

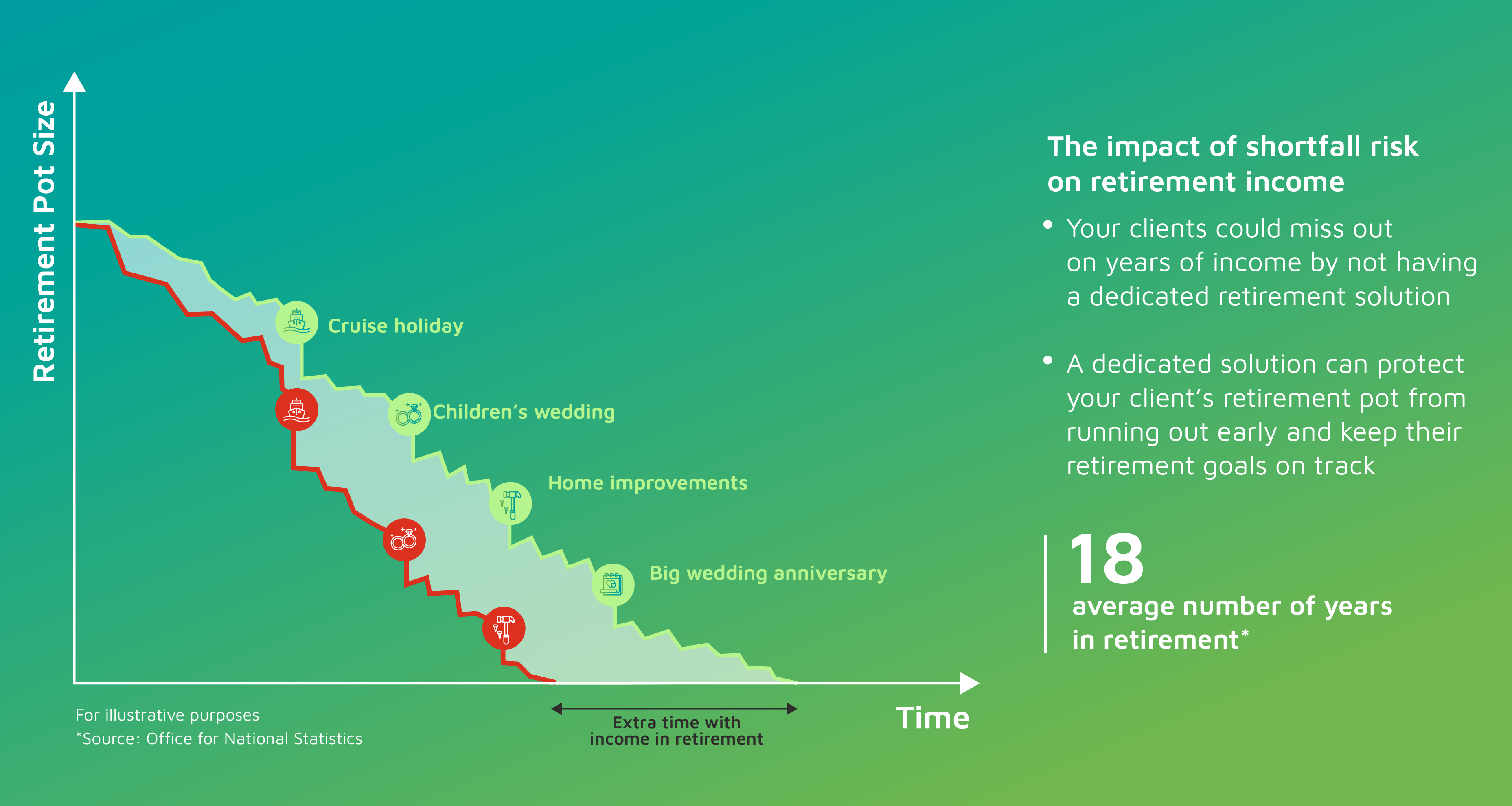

Shortfall risk, where a retirement pot runs out and is unable to provide an income for the entirety of retirement, is one of the primary risks associated with retirement planning, along with sequencing risk. As a result, it is crucial for any adviser to look at the long term options for their client as they approach the decumulation phase of their investment journey and prepare accordingly.

With over-85s being the fastest-growing segment of the UK population and recent studies showing that expected retirement spending profiles often rise later in retirement (Institute for Fiscal Studies, 2022), planning for shortfall risk is more important than ever.

Why use a dedicated retirement strategy to mitigate shortfall risk?

Planning for shortfall risk can enable investors to achieve their retirement goals more easily, without needing to find a balance between overall income and life goals. While traditional retirement solutions are able to provide a sustained income for clients in retirement, a dedicated retirement solution can provide a more targeted risk profile and manage risk in a way traditional solutions may not be able to do.

We know that having an appropriate and suitable retirement proposition can help avoid traditional retirement pitfalls and, with millions more expected to retire in the next 10 years (1.1 million of which are expected by the end of 2023 (Office for National Statistics, 2022)), a dedicated solution will be a key part of any adviser's arsenal.

How can FE Investments help?

At FE Investments, our Decumulation model portfolios are built specifically for a broad range of risk profiles and investment terms, and there is greater consistency and control around the asset allocation. The beauty of our approach is that model portfolios of different investment terms can be mixed to meet the specific withdrawal profile and cashflow plan of a client, while also aiming to mitigate shortfall and sequencing risk.

We understand that retirement planning and creating a retirement income portfolio can be a stressful experience for both the client and the adviser, and we want to help.

We have developed our decumulation illustration tool to help advisers show the effects of retirement planning, specific to their client and how our CRP can help alleviate common retirement risks.

Important information

This is a marketing communication, intended for professional advisers only. Not for use by retail investors. It is not intended as a recommendation to buy or sell any particular asset class, security or strategy. The value of investments and the income from them may go down as well as up and you may not get back the amount originally invested. All information is correct as at the date of publication unless otherwise stated. Where individuals or FE Investments Ltd have expressed opinions, they are based on current market conditions, they may differ from those of other investment professionals and are subject to change without notice.

This communication contains information on investments which does not constitute independent research.