What are the benefits of having portfolios designed for different term lengths in your toolkit?

The regulator shows an ongoing emphasis on firms matching clients with suitable investment products that have been designed to meet their particular needs. Financial advisers are adept at gathering customer information and already do lots to ensure that the composition of the recommended investment portfolios truly reflect the risk appetite and personal financial goals of their customers.

Yet, currently, little is done to account for term/time horizon in many investment products available to choose from. Whilst investing in portfolios often means investing for long-term returns, this can sometimes conflict with an investor’s current situation.

Through your clients’ lifecycle, their needs change. Requirements vary depending on the client’s financial situation and goals, as well as from person to person. The risks involved in investing for the short-term (e,g. market risk) vary significantly from risks involved in longer term solutions.

Your role as financial adviser, is crucial in mitigating these risks, by identifying the requirements of the client in the context of their financial future and recommending a suitable investment. Yet, if you don’t have portfolios with differing term lengths available to you, you can only complete part of the puzzle.

Why are term structures important to the investment advice process?

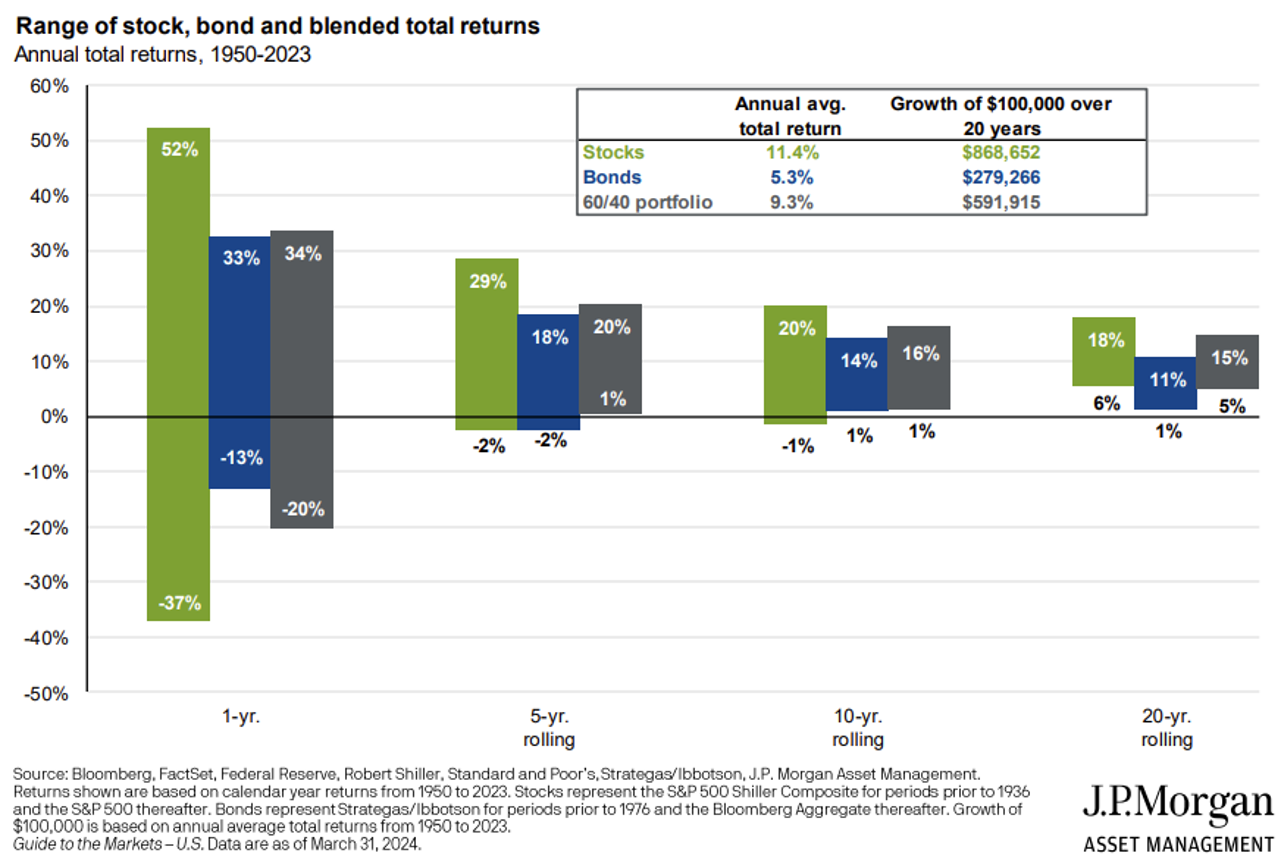

Over time, the variability of return, or possibility of loss, is diminished. As such, when investing for a long time period, it makes sense to favour asset classes which generate the largest returns, despite their variability. In this chart, you can see how risk diminishes over longer periods.

However, this is not suitable for clients who plan withdraw their money sooner. Clients who intend to withdraw money from the market in the short or medium term, do not have the same benefit of time to minimise the impact of fluctuations on the value of their investment and therefore the chances their withdrawal will occur in a negative market are much higher.

To meet their needs, and ensure better outcomes, you need to include portfolios with different term length options, at different risk levels, within your offering. And with Consumer Duty, this seems a clear area in which advisers can avoid causing foreseeable harm to clients who plan to withdraw money within a specific time horizon.

How can FE Investments managed portfolio service help?

Because we believe in the importance of portfolios designed for different investment terms, we offer term structured portfolios across our Mosaic, Hybrid and Responsibly Managed ranges at each risk level.

As they are designed for investors based on the length of time their wealth is intended to be invested, they directly impact your capability to meet the suitability needs of each of your clients. There are three different time horizons at different risk levels - short-term, medium-term, and long-term at the following suggested time periods:

- Short-Term: 3-7 Years

- Medium-Term: 8-15 Years

- Long-Term: 16-25 Years

Find out more about term-weighted, managed portfolios from FE Investments.

The benefit of offering short-term portfolios

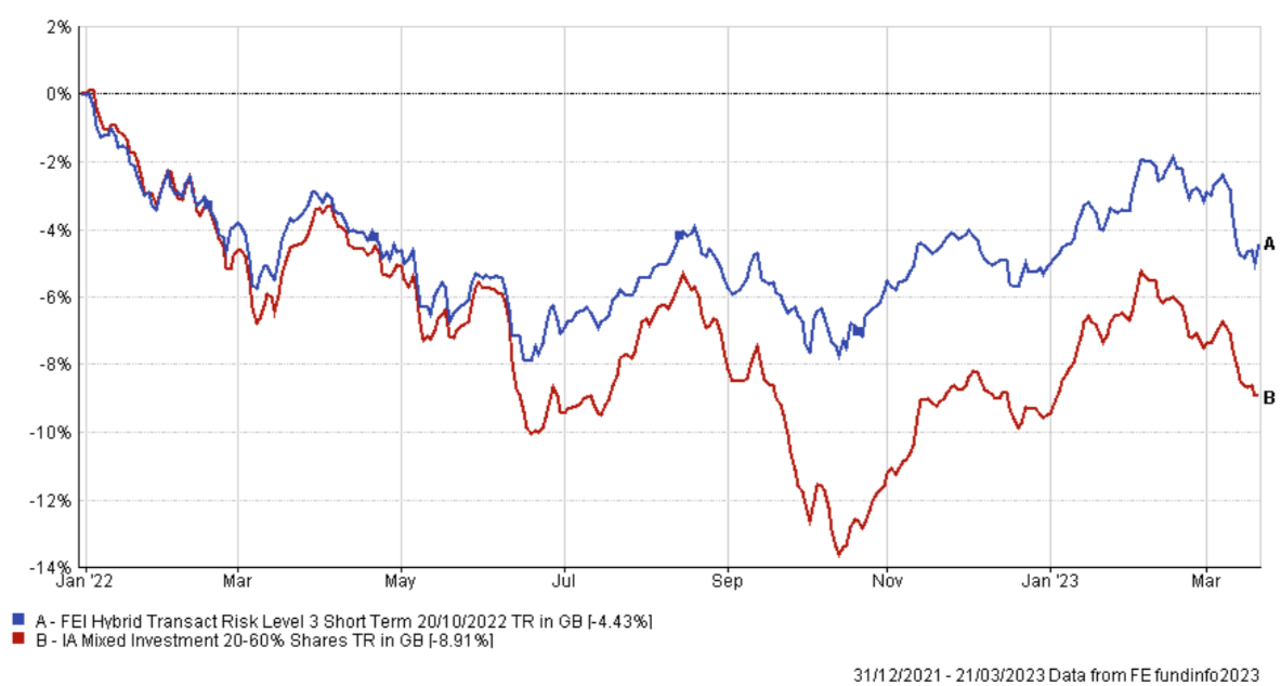

Our short-term portfolios have a focus on limiting the maximum drawdown, the maximum peak to trough, of a portfolio. For example, tighter financial conditions in 2022 troubled markets. Equities and bonds both performed poorly which led to many portfolios falling in value. These are the types of conditions for which the short-term portfolios are designed to preserve capital.

Since the start of 2022, FE Investment Hybrid 3 Short is over 4% better than the benchmark. Over the last two years it limited the maximum drawdown to -8.46%; whereas the IA 20-60% sector reached -13.77%. This represents an extra 5% of portfolio value that we protected.

Of course, this is balanced against how the portfolios perform when markets are rising. The higher allocation to the money market means the short-term portfolios have lower volatility and lag when equities are performing well. The important thing is equipping yourself with the right portfolios to be able to recommend the right investment to each client and improve their outcomes.

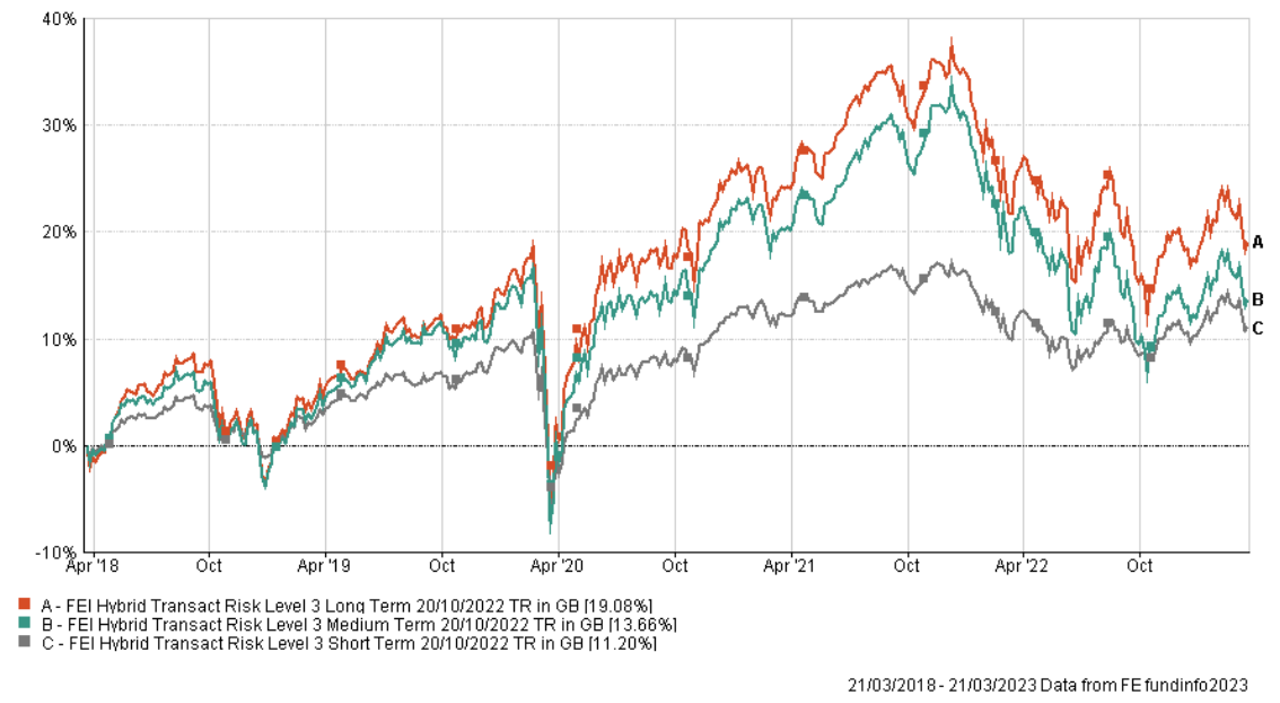

The short-term portfolios

With a focus on minimising volatility built into the short-term portfolios, they exhibited less extreme peaks and troughs over the 5-year period from 2018 to 2023. Over a longer period the portfolios would be expected to lag given they take less risk. You can see this is the case when markets across the board were growing following the covid sell off.

Client outcomes

Short, medium and long-term can be subjective, and sometimes time horizons blur. The skill of the financial adviser is understanding your clients’ requirements and helping them achieve their financial goals through matching them to an investment option built for this.

Recognising what events are upcoming for your clients and factoring this into your recommendation should be a significant part of this. Are they looking to buy a house in the next five years? Is this pot of cash going to be used for children’s school fees? Protecting capital value is crucial in these scenarios.

Yet, without portfolios that have been designed for differing term-lengths, advisers are missing what is a crucial part of their investment solutions toolkit when it comes to ensuring suitability and avoiding foreseeable harm.

Important information

This is a marketing communication, intended for financial advisers only. Not for use by retail investors. It is not intended as a recommendation to buy or sell any particular asset class, security or strategy. The value of investments and the income from them may go down as well as up and you may not get back the amount originally invested.