The end of June saw the first major milestone for large asset managers’ mandatory TCFD-aligned reporting in the UK. Those managing more than £50 billion – which the Financial Conduct Authority (FCA) judged to include 34 groups – should have published their first entity-level reports in line with the TCFD recommendations, based on calendar 2022 data.

Product-level TCFD reporting is following shortly after, with more on that below.

Asset managers and asset owners with over £5 billion should now be compiling their data for 2023, ready to publish their first reports by June 2024.

Where did this come from?

The Financial Stability Board established the Taskforce on Climate-related Financial Disclosures in 2015 to develop a set of recommendations on the disclosures companies should make to help investors and others to assess the risks of climate change.

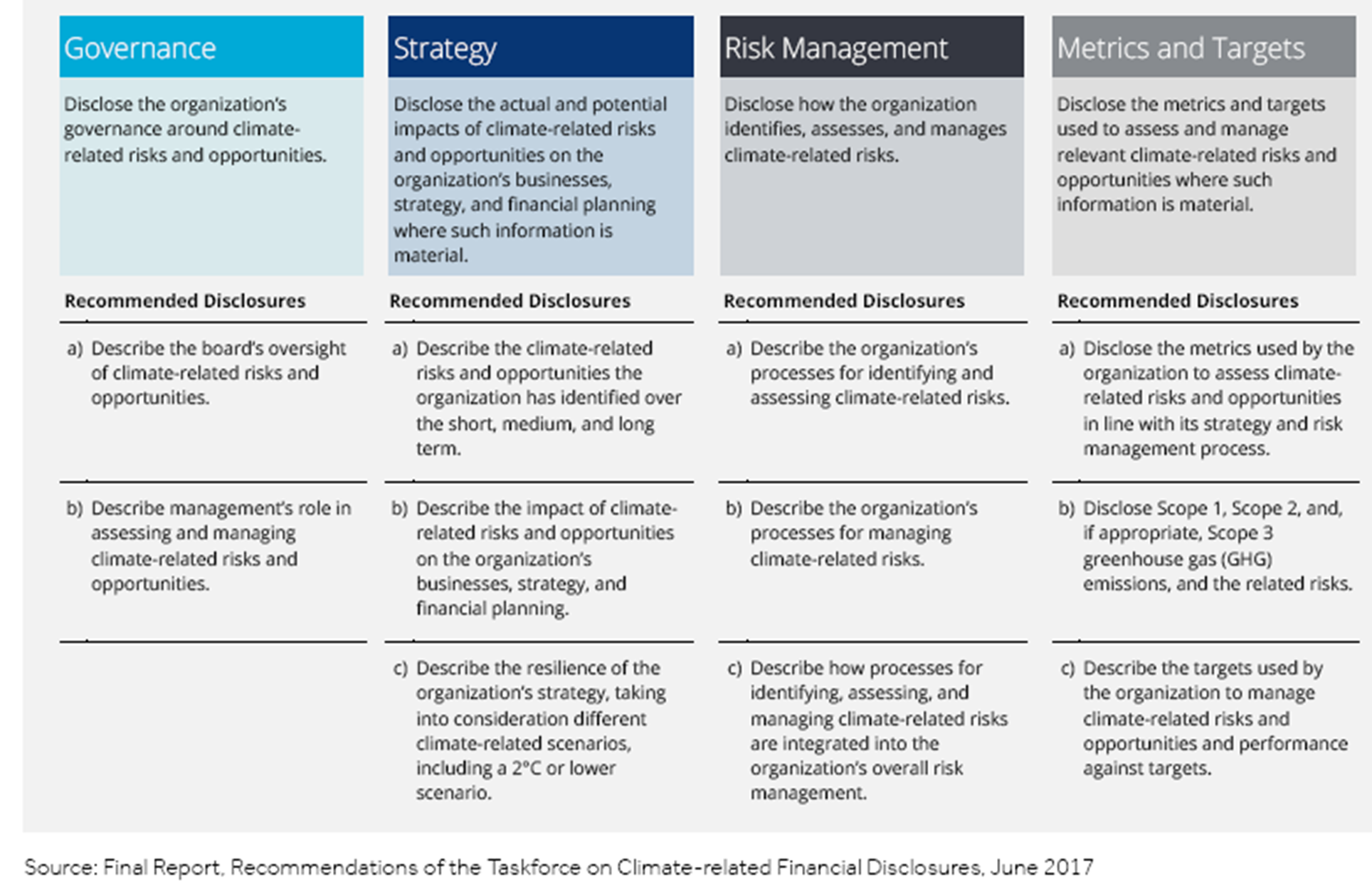

The TCFD’s eleven recommendations were published in 2017, divided into four categories – governance, strategy, risk management, and metrics and targets.

HM Treasury adopted the TCFD recommendations as the baseline for disclosures by listed companies, asset managers and asset owners in its 2020 roadmap, to be implemented by the FCA, the Department for Work and Pensions (DWP) and the Bank of England.

The eleven recommendations, in those four categories, are

Product-level reporting

For reporting purposes, “products” include authorised funds and pension schemes, and the climate-related reporting for those products includes metrics such as weighted average carbon intensity, with additional disclosures if the product’s climate-related approach differs materially from the entity-level disclosure. The product-level disclosure must be included in the fund’s first annual or half-yearly report or periodic client report or pension benefit statement after the 30 June deadline, starting in the year the entity-level report is due.

It is also worth noting that clients who need to publish their own climate-related disclosures may request an on-demand report, in which case the firm must provide that report “within a reasonable period of time and in a format which the firm considers appropriate to meet the information needs” of the requesting client. This report should cover either the latest data available or a period agreed between the parties.

Going forward

The FCA said in its consultation on Sustainability Disclosure Requirements (SDR) that it planned to incorporate the standards set out by the International Sustainability Standards Board (ISSB) into its disclosure requirements for asset managers and funds once they are finalised.

The first two sets of ISSB standards were published in June and are expected to be endorsed by the International Organisation of Securities Commissions (IOSCO) in time to be applied from 2024.

The FCA is also expected to publish its policy statement and final rules on SDR by the end of September, so it should then be clear how the TCFD recommendations, the ISSB standards and any other metrics will fit together in asset managers’ sustainability disclosure requirements.