TCFD is dead, long live TCFD, ISSB, TNFD…

When the Taskforce on Climate-related Financial Disclosure (TCFD) was set up in 2015, it was charged with coming up with guidance on how to assess the risks associated with climate change on companies.

This was to give investors, insurers and lenders the tools they needed to more accurately price in the impacts that climate change could or would have on their operations, which would in turn make for well-functioning efficient markets.

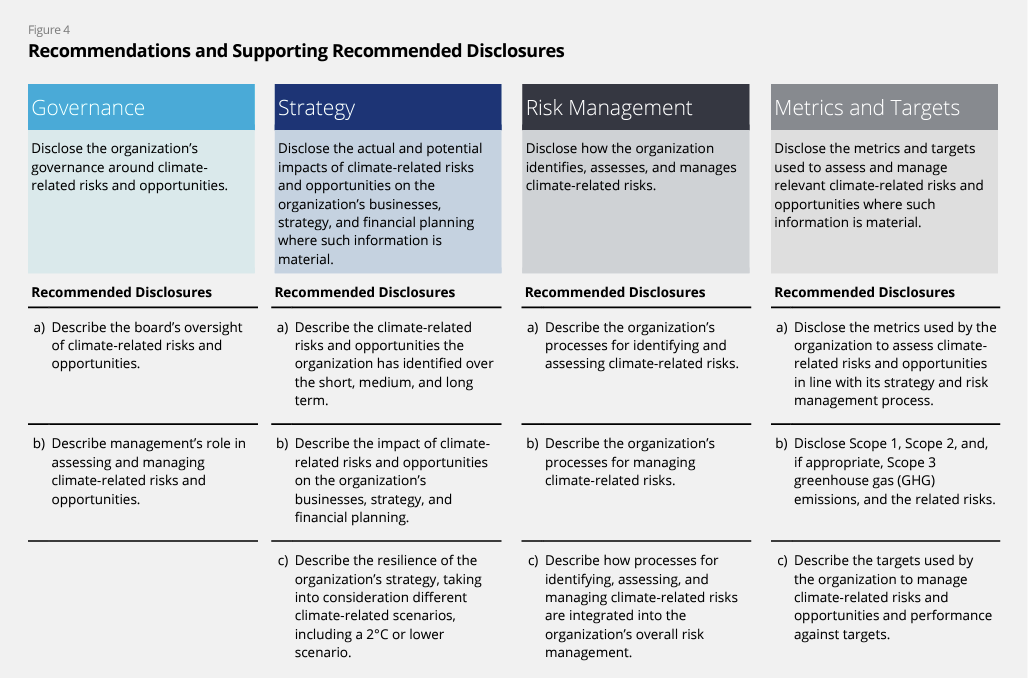

In 2017, the TCFD published 11 recommendations, broken down into the four pillars of governance, strategy, risk management, and metrics and targets, which focus on the opportunities presented to companies by climate change as on the risks.

During 2020 and 2021, the UK government and the FCA adopted the TCFD recommendations for their climate-related disclosure requirements by listed companies, limited liability partnerships, private companies, workplace pension schemes, asset managers and asset owners.

The TCFD was never intended to be a standard-setting organisation so the recommendations were never intended to be reporting standards. Apart from requiring firms to disclose their greenhouse gas emissions and other climate-related metrics they may adopt, the recommendations required organisations to describe elements such as the risks and opportunities they had identified, the board’s oversight of those risks and opportunities, and their impact on the organisation’s strategy.

Moving, on, the International Sustainability Standards Board (ISSB) was established to develop the TCFD recommendations into corporate reporting standards that could be used consistently both by companies and the funds that invest in them.

At the end of 2021, the FCA said in its discussion paper on Sustainability Disclosure Requirements (SDR) that the then unpublished ISSB reporting standards would “form a core component of the SDR framework”.

Within the FCA’s remit, the first obligation was for asset managers with over £50 billion under management and asset owners (life insurers and pension providers) with over £25 billion to publish TCFD-aligned disclosures at the entity level for calendar 2022 by the middle of 2023. Asset managers and asset owners with over £5 billion of assets follow suit a year later.

In each case, once an entity has come in scope of the entity-level disclosure requirements, they also need to follow those with product-level disclosures by the time of the next annual or half-yearly report.

So, at the time of writing, large asset managers and asset owners should by now have published their first entity-level disclosures and be well in their way to publishing product-level disclosures, while smaller organisations should be building up their data for publication by the middle of 2024. Any institutional investor needing to publish its own TCFD-aligned disclosure can also request an annual on-demand report to meet its own reporting requirements, covering an agreed time period.

While all of this has been going on, the Financial Stability Board (FSB) announced that the TCFD would be wound up after it has published its 2023 progress report, having confirmed that the ISSB would take over responsibility for monitoring climate-related disclosures from 2024. As the TCFD says it was only ever set up as a temporary body to lay down the high-level principles, this could all be seen, with hindsight, to be part of the plan from the start.

With the ISSB standards having grown out of the TCFD guidelines, those guidelines are clearly not going away. Rather, they have been formalised into a set of reporting standards. They also formed the basis of the recently launched 14 recommendations from the Taskforce on Nature-related Financial Disclosures, or TNFD, which are divided into the very slightly amended pillars of governance, strategy, risk and impact management, and metrics and targets. Instead of disclosing greenhouse gas emissions as part of its climate-related disclosures, organisations should disclose the metrics they use to assess and manage material nature-related risks and opportunities, and their dependencies and impacts on nature.

In last year’s consultation paper on Sustainability Disclosure Requirements (SDR) and investment labels, the FCA said that TCFD was its baseline for disclosures, but even then, several months before the first ISSB standards were published, said that they would be brought into the mix when they were finalised and adopted.

The ISSB standards were endorsed by IOSCO, the global regulatory overseer, in July, so the expectation is now that the ISSB standards will become the baseline when the SDR policy statement and final rules are published towards the end of this year and come into force a year later.

While, on the face of it, all of these developments could imply that the need for asset managers and asset owners in phase 2 of the TCFD disclosure roadmap (those with over £5 billion of assets) could scrap their plans, that is definitely not the case, for two reasons.

First, the TCFD is not quite dead yet and won’t be until it has published its 2023 progress report, covering the period these groups need to report on. Second, the ISSB standards that are coming in from 2024 rely heavily on the TCFD recommendations, so while the organisation may not be with us for much longer, those recommendations certainly aren’t going away.

{kind=link}

---

Mikkel Bates, Regulatory Manager, FE fundinfo

This article first appeared in IFA Magazine on 27 September 2023